South Africa - Personal

South Africa - Personal

“Only a crisis – actual or perceived – produces real change. When that crisis occurs, the actions that are taken depends on the ideas lying around.” – Economist Milton Friedman

A WELCOME, BUT UNLOVED, RECOVERY

Financial markets around the world rebounded in the second quarter of 2020, restoring a large portion of the decline in asset values during February and March. The market revival occurred despite the widely held view that the economic recovery from the damage wreaked by the virus and the response thereto will be slow and painful in many parts of the world, especially in South Africa. The strongest driver of the market outcome was the unprecedented level of fiscal and monetary stimulus unleashed by governments and central banks around the world. Globally, governments have implemented fiscal support of more than 7% of GDP, compared to the International Monetary Fund’s June forecast of a global economic contraction of -4.9% in 2020. So far, at least for financial markets, the economic life support has worked.

The recovery in equity markets was narrow. Global technology companies — obvious winners given the forced behavioural changes in response to the pandemic — have materially outperformed the broad market indices. In the US, the S&P 500 is at the time of writing flat for the year to date, while the major technology companies are up nearly 50% this year. Smaller companies are languishing, with the Russell 2000 Index still down 12%. Locally, Naspers (+35% this year) and Prosus (+52%) have performed much better than domestic bellwether businesses such as Shoprite (-18%) and Sanlam (-22%).

The number of unknowns remain high in the current environment. The interplay of the massively contrasting forces of an unprecedented economic recession and unprecedented stimulus will continue to drive markets. Uncertainty is increased by rising inequality and more social unrest around the world. Covid-19 has accelerated the future, turning historically investable businesses into value traps, and higher debt levels everywhere increase risks. Given this challenging backdrop, we continue to focus on protecting our clients’ capital and growing their wealth by building resilient, diversified portfolios with a long-term view. For an example of how this plays out in practice, read Sarah-Jane Alexander’s article, explaining how we used the market dislocation to improve the quality of the domestic equity holdings included in your funds.

NOT THE RESULT WE HOPED FOR

During April, all of us were concerned about the then emerging implications of the pandemic, but still hopeful that South Africa could get ahead of the virus. Sadly, we now know that we have not achieved this positive outcome. We appear on an unwanted leader board, with the fifth-highest number of total confirmed Covid-19 cases globally. With 0.8% of the world’s population, we have 3% of the confirmed active cases. One positive is that we have a young population, with an average age of 27 compared to Europe’s median age of 43 years. This means that, despite a raging epidemic, our death rate is still in line with our population share.

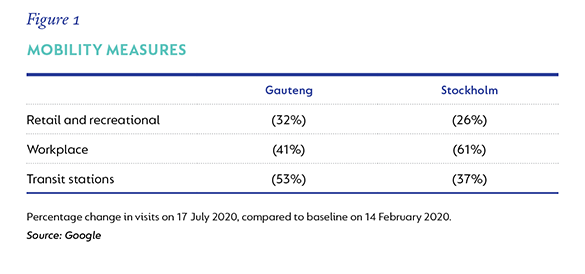

At the same time, we have paid a material economic cost. As Marie Antelme points out here, we expect the domestic economy to contract by nearly 10% this year, complicating the already very challenging fiscal arithmetic facing the National Treasury. While some of the economic pain resulted from policy errors made by government, the pandemic is the primary driver of the damage. A small example can be found in comparing recent Google mobility data for South Africa and Sweden’s capital Stockholm, where a hard lockdown was not imposed and where the active cases are a fraction of ours. Figure 1 shows how much lower than the pre-Covid-19 baseline activity levels in Stockholm still is — not very different from the situation in Gauteng.

While we wait for a vaccine, the only viable response we have is a combination of hygiene, distancing and wearing masks, as we implore you to do on the cover.

RETURN EXPECTATIONS

We recently concluded our annual investor survey, primarily aimed at understanding how you feel about the investments you have entrusted to us. A key survey question is what the return is that you expect from your portfolio over time. Our aim is to understand how well the expectations of investors with different needs and time horizons calibrate to what we think the likely future market outcomes will be.

My first observation is that more than 25% of you said that you just don’t know, which is the highest level of uncertainty since our first survey four years ago. This is understandable, given high volatility levels and the disappointing performance of domestic growth assets in recent years.

Overall, expectations have declined and 61% of the investors who expressed an opinion expect an annual return over time of 10% or more today, compared to 82% in 2017. Most of this decline can be ascribed to investors with a long-term growth goal, which is the cohort most likely to be exposed to the asset classes that disappointed over the last five years.

The average long-term growth return expectation is 10.9% per year (2017: 12%). Coronation’s expected return forecast for a multi-asset fund, such as Balanced Plus, over the next decade is in the 9% to 12% range given current valuation levels across the different asset classes, and assuming that we manage to add around 1.5% annual outperformance to the benchmark. For long-term growth investors, we think expectations, albeit on the optimistic side, is achievable.

The situation is different for investors with needs consistent with the funds that have done well over the last five years. Investors with international diversification as their primary goal have unchanged return expectations of 11.8% per year (2017: 11.6%). This is also the case for those with immediate income needs (which the Coronation Strategic Income Fund is aimed at), who expect 9.3% p.a. (2017: 9.0% p.a.).

We think these expectations may be heroic. The S&P 500 had a golden decade, returning 13.6% per year in US dollar compared to the 119-year average return of 6.5%. The return over the last decade was fuelled by declining tax rates and lower interest rates, which allowed profit margins to widen and discount rates to drop. These tailwinds are not likely to blow as strong over the next 10 years. The US still makes up 58% of the MSCI All Country World Index, the most important benchmark for global equity funds. While the international investment universe offers many opportunities to add outperformance which may help to get closer to expectations, we expect global index returns of 7% to 9% per annum over the next decade.

Our key concern relates to investor expectations in the immediate income category. Income investors typically have shorter time horizons, often of two to three years. Policy interest rates, anchored by prevailing inflation, play a major role in return outcomes for these investors. Given the demand destruction caused by the pandemic, inflation declined to 2.1% in May, a 16-year low. We expect inflation to remain around the lower end of the 3% to 6% target range over the next three years.

The South African Reserve Bank has already cut interest rates materially, and given how weak the economy is, further cuts are likely. Over the next three years, we think that returns in the 5% to 6% range will be a good outcome for income fund investors, which is much lower than the 9.3% survey expectation and the 8.4% Strategic Income delivered over the previous decade. While investors could successfully ride out the storm in lower risk funds historically, the outlook for adopting this approach as your long-term strategy is less rosy.

OPPORTUNITIES AMIDST THE THREATS

As a country, we find ourselves in a tough situation. For those old enough to remember, conditions feel as daunting as in the late 1980s, hallmarked by a state of emergency and brutal policing in the townships, a low-intensity civil war in KwaZulu-Natal, sanctions, government’s inability to pay its foreign debt on time and the enforcement of prescribed assets and strict capital controls. Yet we managed to step back from the cliff edge and entered a long period of growing prosperity over the next two decades as South Africa reinvented itself. As Milton Friedman concluded in the second part of the quote at the top of this Inbox, we need to make sure that we are ready with alternatives to existing policies, to keep them alive and available until the politically impossible becomes the politically inevitable. We will, through our own actions and engagement with government as part of organised business, continue to do our part to try and influence the direction of travel onto a more constructive path for our country and all of its people.

We remain committed as always to provide you with investment and service excellence. If you have any concerns, questions or issues, please do contact us via clientservice@coronation.com. We hope you and your loved ones stay safe and healthy.

Explore Investment Insights on the global economy, markets and topics related to our business.

Subscribe to our Corospondent newsletter